Kudos to The Star, well Star Business and Tan Sri Lin See Yan to be precise, over the article - Bitcoin: Utter pipedream - Business News of 10 February 2018

In my post Chart: Follies With Tulips & Bitcoins of 21 December 2017 on my IT.Scheiss blog, I wrote the the exuberance and euphoria over cryptocurrencies about one and a half months back reminds me of similar wild exuberance, hype and euphoria in the period back in 1998 and 1999, before the DotCom Bust of 2000, and that I my gut feeling was that with 1,368 crypto currencies listed on CoinMarketCap.com aorund 21 December 2017, there will not be enough money in the world to raise the values of all these digital alternative fiat currencies as high as the price of Bitcoin at the time as crypto-gamblers switch to one or more of the increasing number of other cryptocurrencies, thus causing the respective prices of all cryptocurrencies to average out towards a lower level and also that it looks like the cryptocurrency craze is heading towards a "DotCom Crash 2.0" about 20 years after the first DotCom Crash.

My gut feeling remains the same today when as of 11 February 2018, 05.54 hours Coordinated Universal Time (UTC), there were 1,523 cryptocurrencies listed on Coinmarketcap.com or 155 more in about one and a half months.

Bitcoin was created as an alternative currency independent of the control of establishment national and international currency regulators and of the establishment banks, following the 2008 financial and economic crisis (and the bailout of the "too big to fail" banks, which President-elect O'Bummer agreed with in late 2008 - so much for a "president of the people") and that the distributed Blockchain ledger technology behind it put its control in the hands of the "the people" - or more precisely, the people who have enough funds and resources to afford the huge computer farms,powerful computers and for the electricity to process the complex algorithms to create more Bitcoin (a process called "mining" in simple terms), as well as those with enough funds to buy and sell Bitcoin as people do shares on stock markets. This certainly isn't something which the plaebian masses can play in - it's a big boys game.

Once the emphasis shifted to the exchange rate of Bitcoin with establishment currencies such as the U.S. dollar, Bitcoin ATMs and so forth, that was when Bitcoin proverbially lost its virginity as an independent, alternative currency, fell from grace and became just a part of the established capitalist currency system, fiat or otherwise.

And today, Bitcoin and other cryptocurrencies have become assets to be speculated upon and traded on markets, just as shares and commodities are speculated upon and traded.

As an individual, very small time, retail investor and trader on the share market, I understand the importance of studying the fundamentals behind each share, such as the healthy revenue and profit track record of the company over the past three to five years, prospects of continued or increased future revenue and profitability due to expansion, penetration into new foreign markets, tenders and contracts won recently which would result in greater revenue and profitability; as well as the technical indicators of its share price movements which reflect the speculative forces acting upon its share price, such as an increase in its share price in the period pending acquisition of some of its units by another company or in the period between the closing of its books and the release of its quarterly or annual report, where a rise in its share price reflects anticipation of better quarterly results, whilst a falling share price before the estimated release of the quarterly or annual report reflects expectation of poorer results.

In stock trading terms, an investor is one who bases ones share purchases and sale based primarily on the company's underlying fundamentals, whilst a trader is one who bases one's purchases and sales of shares based upon speculation, often aided by the movement of technical indicators, especially the movement of graphs of short, medium and long term moving averages relative to each other, as well as more complex indicators such as Fibonacci Retracement, Elliot Waves, previous highs (resistance levels), previous lows (support levels), candlestick patterns and so forth.

However, an astute stock trader will first do all due diligence research to ensure that the fundamentals behind a stock are sound, then buy when a share price is relatively low and well before the latest quarterly or annual report is released, then ride the share price upwards until the indicators show that its uptrend is weakening and is likely to turn down, then sell and lock in one's profit. On the other hand, if the price of a company's share begins to trend downwards in the lead up to the release of the next quarterly or annual report, a wise trader will stay clear, since this is an indication of a poor report.

I good place to do a quick check on the fundamentals of companies listed on Bursa Malaysia is MalaysiaStock.biz

Yes, there are speculative forces which act upon the intrinsic value of a company's stock which drive it up and down around its intrinsic value based upon fundamentals but a wise stock trader who "plays" the stock market will ensure that the companies whose shares he or she "plays" in have strong underlying fundamentals or can likely get burned badly like gamblers in a casino. Usually, the prices of the shares of companies with sound fundamentals are less prone to wild fluctuations in share price - i.e. volatility.

When it comes to fiat establishment currencies, such as the U.S. dollar, whilst their value is not tied to tangible assets such as gold or silver, however their exchange rate vis-a-vis other national currencies reflects the fundamentals of the economy of the country issuing them, so their exchange rate is like the price of a company's share - based upon fundamentals as well as the speculative forces acting upon them.

Now with the exception of some cryptocurrencies which are backed by gold, silver or other tangible assets, the prices of cryptocurrencies, most of which are also fiat, are driven purely by speculative forces, hence their great price volatility.

The chart of the price of Bitcoin on Coinbase.com below shows that its price peaked at US$19,206 on 18 December 2017, resulting in all the exuberance and euphoria in December last year but its price had dropped to US$6,036.92 on 6 February 2018 and has since rebounded to US$8,088.53 when this screen cap was taken today 11 February 2018.

Yes the price of Bitcoin rebounded since 6 February 2018 and rose to above US$8,000 but its price has been "going sideways" in stock trading terms and this rebound is showing signs of losing steam and is heading southwards.

Whilst nothing is absolutely certain, nor permanent with share and commodity prices or foreign exchange rates, however this looks like the Bitcoin price is going through what stock, commodity and currency traders call a "dead cat bounce" (see chart below) in the short or medium term at least.

There appears to have been an inverse correlation between the price of cryptocurrencies and the Dow Jones Industrial Average (DJIA) stock market index (based upon the prices of shares of 30 large companies on the New York Stock Exchange and NASDAQ), since some investors who sold their shares on the NYSE or NASDAQ following the plunge of the DJIA since 1 February 2018, had sought "refuge" in cryptocurencies instead or some intending investors decided to speculate on cryptocurrencies instead whilst stock prices were on a downturn.

Well these speculators who think that cryptocurrencies such as Bitcoin are a "safe haven" may well be hit by a double whammy if their price drops further.

If you want to play in the game of finance capitalism, be prepared to get burned and burned badly.

How about going back to play that board trading game Monopoly, with real fiat Monopoly money? At least that's not a load of IT scheiss.

These starry-eyed anarcho-capitalists and libertarians thought that they could solve the problems with central banks such as the U.S. Federal Reserve, Bank of England, Bank Negara Malaysia, international banking regulatory institutions and so forth through creating an alternative, fiat, digital, cryptocurrency in parallel to the establishment currency system, and as always has happened, the establishment, capitalist and imperialist currency system co-opted the alternative systems, as has often happened with other alternatives such as whole foods, organic foods, alternative medicines, alternative music and so forth, which were co-opted by established food processing, pharmaceutical (big pharma) and music corporations.

Perhaps most of them are anarcho-opportunists out to sucker many well intentioned but naive techno-Utopians into getting caught up in this crypto-Ponzi scheme.

Whilst admittedly difficult, the solution to the problems in the establishment currency system is to confront the problems head on and fix the problems within the establishment currency system - and that requires political will.

At the end of the day, let me get one thing clear - the DotCom Bust of 2000 did not see the end of dotcoms but a massive shakeout of the majority of dotcoms, leaving a handful, such as Amazon.com, Google, Facebook and others to fill the void and come to dominate the Internet today. Likewise, "DotCom Bust 2.0" or let's say when it hits, Crypto Bust 1.0 will see a massive shakeout of cryptocurrencies, leaving a handful, including perhaps Bitcoin to dominate the "alternative" financial space and we the plaebian masses will be beholden unto them, just like how we are beholden to Google to yield us our search results today, as well as to Facebook, WhatsApp and an handful of other social media sites, even though we don't quite like it.

Also, like those You Tube content creators who vehemently and strongly objected and criticise You Tube on You Tube itself, for demonetising their videos deemed inappropriate by You Tube's algorithms, yet they have no choice but to tenaciously hang on to You Tube, since there are no other platforms which are as lucrative or provide them with as much exposure for their views as the now dominant You Tube does.

Like right libertarian "Styxhexenhammer666" complains about You Tube on You Tube

And Canadian Maoist You Tube commentator Jason Unruhe

Earlier Jason had even stronger words for You Tube on You Tube.

Jason admits to him being in a part-time, lowly paid job in the services side of the much touted information and services economy.

So much for the Internet empowering the little guys to compete on a level playing field with the big corporations, when over the past 20 or so years, a handful of little guys have pushed aside the rest to become giant corporation dominating the Internet.

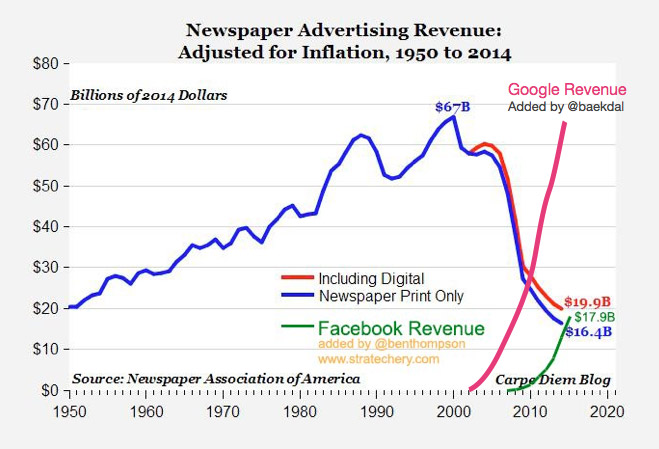

Besides that, these big Internet guys have been sucking away advertising revenue from print, online and digital publications around the world, especially where fixed and mobile broadband penetration are high enough, including in Malaysia and Singapore, where newspapers are in trouble, and some online only publications have gone under, unless they have a rich sugar daddy or sugar daddies who continue to prop them up financially.

As for me, I'm staying far away from this crypto-casino craze but will watch as the proverbial shiess hits the proverbial fan and those who continue to have faith in this crypto-scheiss get badly burned.

The Star's article referred to follows below.

Yours most truly

IT.Scheiss (A HiTekHeretik)

===============================

Bitcoin: Utter pipedream - Business News

by lin see-yan - what are we to do?

I JUST returned from a meeting of the Asian Shadow Financial Regulatory Committee in Bangkok.

The group comprises Asian academic experts on economics and finance. Their role is to monitor the state of the world economy and the workings of its financial markets in the light of existing and prospective policies; and draw lessons and give advice on vital public policy issues of current interest to regulators and market practitioners to make the world a better place.

The group comprises 23 professors from 14 countries, coming from a diverse group of universities and think-tanks, including the universities of Sydney and Monash, and of Fudan, Hong Kong and Sun-Yat-Sen in China, Universitas Indonesia, universities of Tokyo and Hitotsubashi, Yonsei and Korea universities, Sunway University, Massey University in New Zealand, University of the Philippines, Singapore Management University, National Taiwan University, Chulalongkorn University and NIDA Business School, University of Hawaii and University of California at Davis, University of Vietnam, and Tilburg University in the Netherlands.

They examined key issues surrounding the theme: “Cryptocurrencies: Quo Vadis?” focusing on the role and activities of the flavour of the month, bitcoin. At the end of it all, they issued the following statement:

“Cryptocurrencies in general, and bitcoin, in particular, have been receiving considerable press of late, driven mainly by wide swings in value in the cryptocurrency exchanges. There are now in excess of 2,500 products considered to be cryptocurrencies and in the last three weeks alone their combined market value has plummeted from US$830bil to US$545bil as of today, of which US$215bil is attributed to bitcoin and bitcoin cash.

To keep this in perspective, however, Apple Inc has a market value of US$880bil as of today. Market value measures the equity value of a business – or what investors are willing to pay for its future profits. Unlike enterprises, however, bitcoin has no business, no intrinsic value, no cash flows, no profit and loss statement, and no balance sheet. It is a speculative instrument.

Cryptocurrencies, including bitcoin, are not considered currency today because they are not a universal means of payment, nor a stable store of value, nor a reliable unit of account. Buyers purchase on the basis that these cryptocurrencies would rise in value. While market value has been the main focus of the current interest, the more important issues are around the role of cryptocurrencies both as financial assets, and the role they can play in transaction settlements, and their implications, if any, on financial stability.

While there is much interest in cryptocurrencies, especially bitcoin, the volume of transactions remains very small currently. For example, total US dollars (cash) in circulation amount to US$1.6 trillion as of today. M3 (broad money) is valued by the Federal Reserve at US$14 trillion. Total US economy assets in 2016 were valued at US$220 trillion. So why the fascination with cryptocurrencies? Supporters of Bitcoin claim it to be a superior store of value to fiat money issued by central banks because its supply is limited by design and therefore cannot be debased. In addition, the technology behind bitcoin, called the Blockchain, provides anonymity to its players. That is why it is a favourite with money launderers, tax evaders, terrorists, drug smuggler, hackers, and anyone who wants to evade the rule of law. Many people who use cryptocurrencies assert that they pay minimal transaction costs mainly because it avoids the cost of financial intermediation.

Still, there is large potential for capital gains because of the wide volatility of its price movement. This is the main driving force behind the popularity of cryptocurrencies like bitcoin. However, there are high risks involved including extreme volatility and opaque, unregulated exchanges that are prone to cyberattacks.

Authorities and regulators worry about bitcoin because they fear it is a bubble. In the event of a bust, investors in bitcoin – they are many, spread over various continents and countries – will be hurt; and they exert pressure on governments to regulate this business in order to protect investors.

In addition, they worry about the impact – in the event that cryptocurrency trading becomes a significant element in maintaining financial stability – in terms of the impact on the transmission of monetary policy and on its effects on the banking system, and most of all, on systemic risk, if any.

Authorities have responded in different way. In South Korea, new regulations today require banks and exchanges to identify who their customers are, imposing greater transparency in the conduct of the cryptocurrency business. On the other hand, Japanese authorities are more liberal. They only require the registration of companies engaged in this business at this time.

Many other authorities, including those in the US, are adopting a wait-and-see attitude while studying the issues, recognising that there may be a role for them to introduce some regulatory measures in the event that the volume and price volatility of cryptocurrency transactions become more and more significant.

In the meantime, government and tax authorities feel uneasy about the impact on revenue collection. Other regulators are worried about crowdfunding through ICOs (initial coin offers). Authorities in a number of countries, including the US, have introduced measures to regulate the issue of new ICOs to ensure that investors are provided with the necessary information before making such investments.

At the same time, central banks in many countries are looking into the desirability and possibility of issuing their own digital currencies, including to counter privately-issued cryptocurrencies.

Recommendations:

1. Bitcoin came into prominence because of an apparent lack of confidence in fiat currency. It is imperative that governments and central banks continue to give priority to (i) protecting the integrity of their currencies; (ii) designing policies to contain inflation to prevent it from debasing the currency; and (iii) strengthening their mandate to promote financial stability over financial development, if needed (including ensure fintech development does not undermine confidence). Also, in cases where authorities do not have the power to regulate the cryptocurrency business, they should actively seek such authority where appropriate.

2. Monetary authorities should be open to creating digital currencies rather than confining their money supply to notes, coins and deposits. But they should do so in a transparent manner and only after careful consultation and study.

3. It is the role of government to warn their citizens and investors about the high risk involved, and ensure transparency in bitcoin activity, and not to unduly introduce more and more regulations that will stifle innovative initiatives. Blockchain technology, for example, does have other useful applications apart from the issue of its use in the creation of digital currency.

Investor protection

As we see today, bitcoin and the other cryptocurrencies are not currencies. Mostly, they reflect speculative activity. Hence, investing and transacting in them involve high risks. It is imperative that investors realise this and approach investing in cryptocurrencies with great caution and with as much information as is available to help them manage these risks.

Investors must fully understand that cryptocurrency prices need not necessarily always rise, particularly because they have no intrinsic value, they could just as easily fall. So investors beware: Caveat emptor.”

Update

The following developments are noteworthy:

Columbia’s Prof N. Roubini (Dr Doom) claims bitcoin is not a currency. Few price anything in bitcoin. Not many retailers accept it (even bitcoin conferences don’t accept it as payment). And it’s a poor store of value because its price can fluctuate 20%-30% a day. Worse, he labelled it “the mother of all bubbles” because its claim of a steady-state supply is “fraudulent”.

It has already created thee similar currencies: Bitcoin Cash, Litecoin and Bitcoin Gold. Together with the hundreds of such other currencies invented daily, this creation of money supply is debasing the currency at a much faster pace than any major central banks ever did. Furthermore, bitcoin’s claimed advantage is also its Achilles’s heel – for, even if it actually did have a steady supply of 21 million units, it is not a viable currency because the supply won’t track potential nominal GDP growth; hence, prices will become deflationary – the kind of phenomenon that economist Irving Fisher believed caused the Great Depression.

Indeed, the head of the European Central Bank had since declared to the European Parliament that cryptocurrencies are unregulated and “very risky assets. Their price is entirely speculative”. That’s not what we want or need. It’s a pity the FOMO (fear of missing out) of many retail investors will end them in a wild goose ride!

Over its nine-year history, bitcoin has had five-peak-to-trough falls of more than 70% each. The recent decline offers a dose of reality to new investors – bitcoin dropped to a low US$7,850 on Feb 2 for the first time since November 2017 – crashing 60% from the high of nearly US$20,000 in mid-December. Sentiment has shifted dramatically this year.

On Feb 5, it fell another 4% to US$7,524. Also, the fledging market has taken a number of blows: Facebook has since banned advertisements on it (for being misleading); US Securities and Exchange Commission has accused some latest ICOs as “outright scams”; US and UK largest banks have put up “road-blocks” to financing bitcoins; and the recent Japanese hack theft of 523 million crypto-XEM (worth US$500mil) brought back memories of Mt Gox, which collapsed after a similar hack in 2014.

Arbitrage traders (buying where it’s cheap and reselling where it is dear) have been active – taking advantage of price differentials in multiple places and different times. They call it “capturing the arb”. Hedge funds, high frequency traders and even amateur enthusiasts are giving it a shot. Price divergences can be due to glitches or network traffic jams. In South Korea, exchanges quote abnormally wide prices reflecting high investors’ demand for bitcoin in the face of strict capital controls – giving rise to a “Kimchi premium” (of as high as 50% above US price; now down to 5% as price disparities are swiftly traded away).

Concern over cryptocurrency activity is spreading beyond China, Japan, South Korea and India. This prompted the governor of the Bank of England, who also chairs the Global Financial Stability Board, to voice his unease over the anonymity embedded in blockchain technology underlying their use, especially for illicit activity (including money laundering). He disclosed that it would be on the agenda at the next G20 meeting. Tax authorities have also expressed concern over the under-reporting of capital gains tax.

Bitcoin futures trading on Chicago’s CME and CBoE exchanges have been slow to catch fire – at the pace of a “slow walk”.

What then, are we to do

Reality check: Bitcoin is proving that cryptocurrencies can erase wealth as fast as they create it. In January 2018 alone, it wiped off US$45bil from its US$200bil in market value generated in all of 2017 – the biggest one-month loss in US dollar terms in its short history. Since then, more value is being lost. For most economists and finance experts, they don’t represent an investable asset – there are liquidity issues, safety issues, exchange issues; most of all, they have no intrinsic value.

Can’t realistically put a fix on their fair value. They are for speculators who are prepared to lose everything. Of course, its something else for those who use them for illicit activity (home to criminals and terrorists), including money laundering. Anonymity means you are potentially closing a chain, while at somewhere along it had some illicit activity that cannot see the light of day.

Fair enough, these concern regulators. But we shouldn’t lose sight of the huge range of opportunities presented by the underlying technology – a view shared by many in relation to raising the efficiency of payment systems. Regulators are right to want to regulate crypto but also, continue to encourage innovation on blockchain. As I see it, so far in 2018, bitcoin has been a total dud. The list of factors driving its decline is growing, especially rising regulatory clampdown occurring around the world.

So, the cryptocurrency market has fallen on tougher times. For sure, Bitcoin has been highly profitable for many investors. Indeed, there continues to be strong interest among millennials.

Bottom line: the year so far has been terrible for bitcoin. But the fundamental positive story for crypto appears to remain intact. Protecting consumers should make it harder for charlatans to sell digital dust. There is a point where it goes from “buying on the dip” to “catching a falling knife”. Only time will tell. So, beware!

NB: Following global regulatory crackdown, bitcoin’s price has on Feb 6 fallen to a low of US$5,947, wiping out over US$200bil so far this year. Bitcoin’s market cap is now US$109bil, about one-third of the total crypto market (that’s down from 85% this time last year). The Bank for International Settlements (banker to central banks) has now condemned bitcoin as “a combination of a bubble, a Ponzi scheme and an environmental disaster” (refers to huge amounts of electricity used to create it) and warns it can even become a “threat to financial stability”.

Former banker Tan Sri Lin See-Yan is the author of The Global Economy in Turbulent Times (Wiley, 2015) and Turbulence in Trying Times (Pearson, 2017). Feedback is most welcome.

Awani reported that IMW managing director and founder Datuk Michael Yip has confirmed the purchase of Focus Malaysia, adding that it is IMW's main agenda to make a transition to the digital platform.

Awani reported that IMW managing director and founder Datuk Michael Yip has confirmed the purchase of Focus Malaysia, adding that it is IMW's main agenda to make a transition to the digital platform.